The Student Loan Payment Pause Ends - Prepare for the Horror Stories

The Student Loan Payment Pause Ends - Prepare for the Horror Stories

Are federal student loan servicers ready for their customers?

In a sort of bookend to our very first issue of this newsletter, which focused on a debt collector that also covered student loans, this week we’ll be “commemorating” the end of the long-standing federal student loan payment pause effective tomorrow, September 1, as interest begins accruing on that date and payments will come due again in October. We’ll do so by taking a look at the service providers (aka servicers) that will be taking center stage as borrowers dust off their loan accounts (and bank accounts) and prepare to figure out how to handle the end of the moratorium. A lot has been written about whether or not the moratorium should resume. A lot is also currently being litigated regarding loan forgiveness, at all levels of court. But what hasn’t gotten enough attention, in my opinion, are the servicers who are going to be handling their returning customers (who had no choice in selecting them when they took out their loan). Let’s dive in:

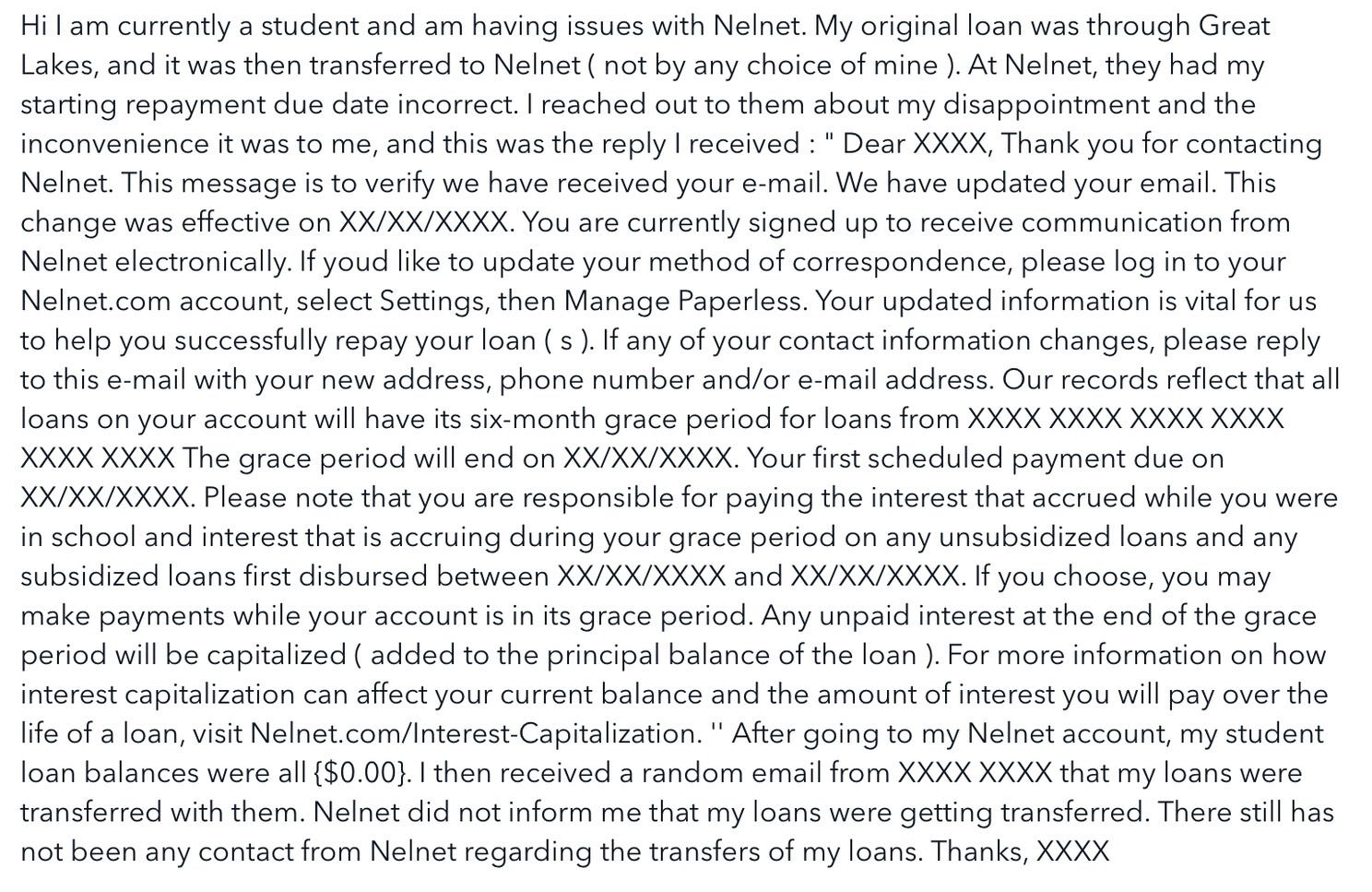

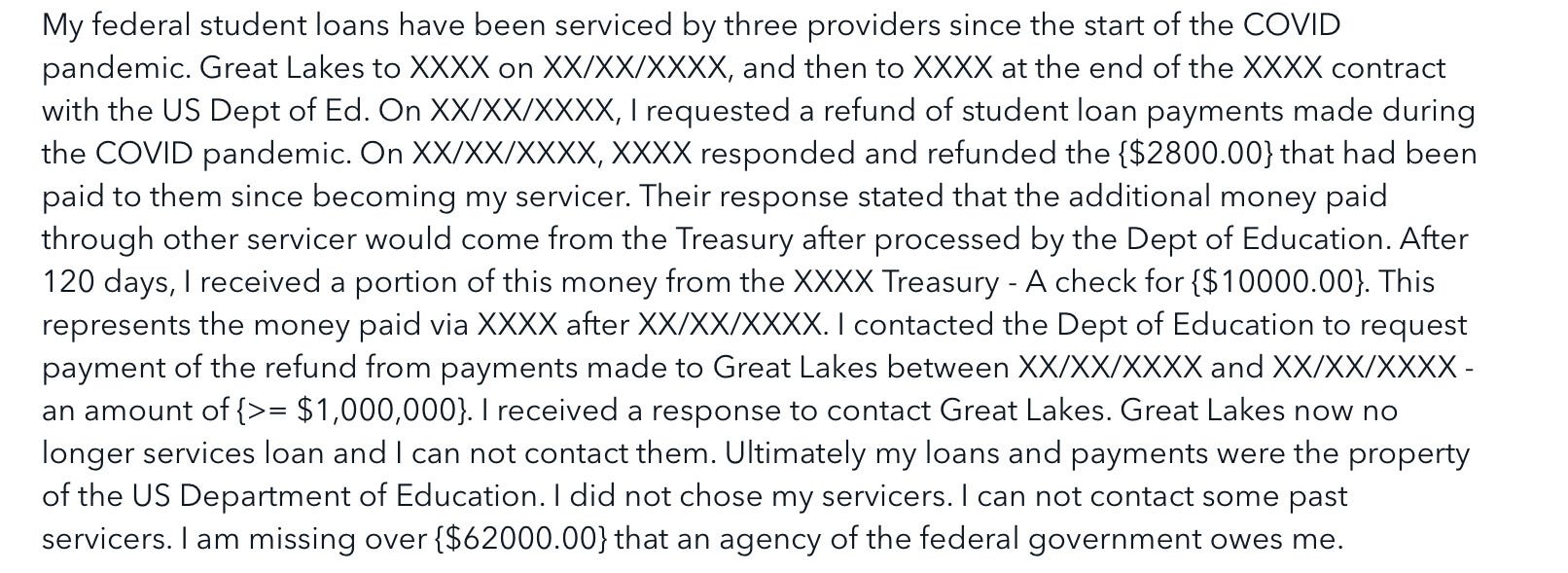

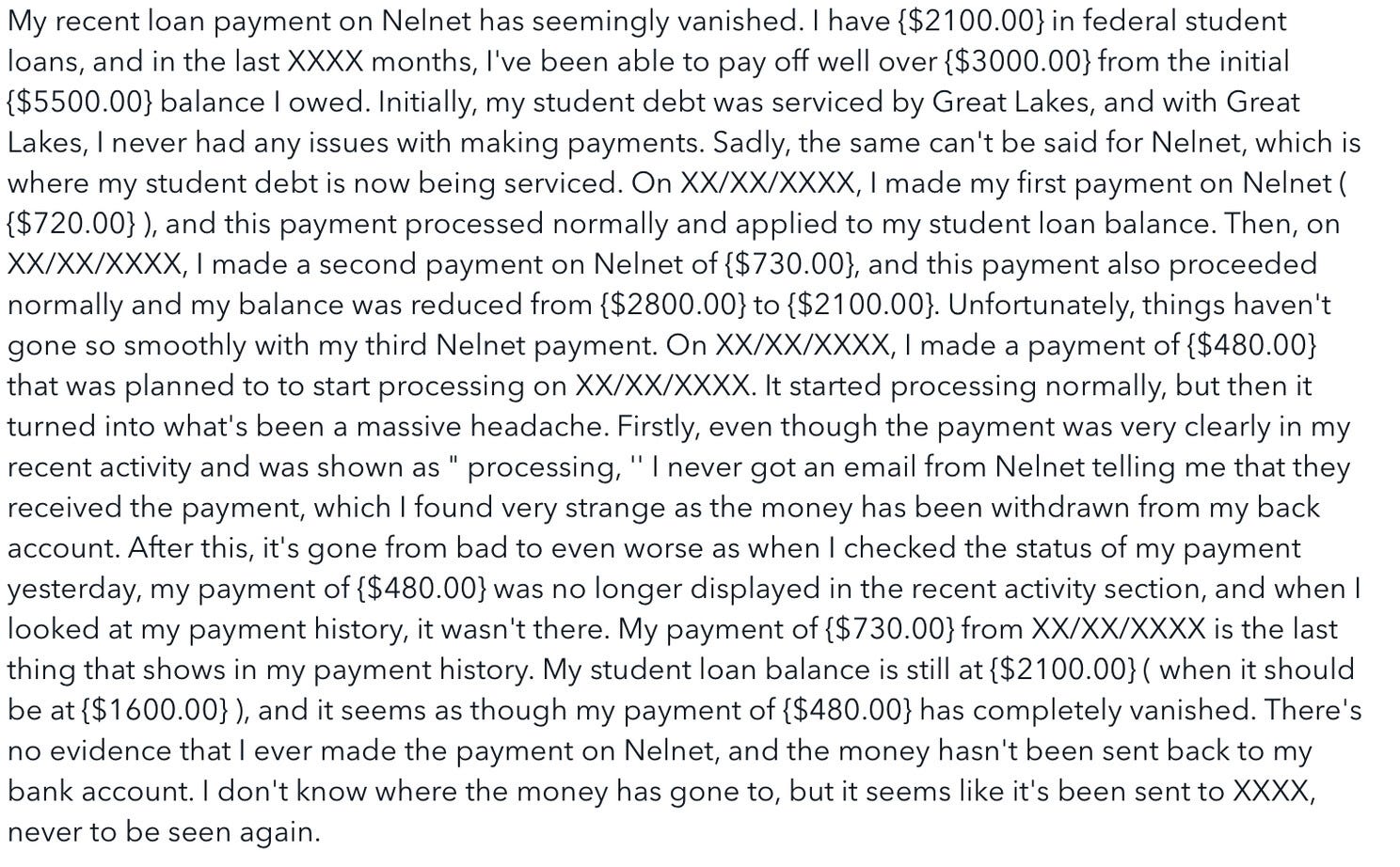

Great Lakes/Nelnet

The Transfer Saga

Both of these servicers were listed as supporting student loans for some time, but as of June 2023, Great Lakes has handed over its entire portfolio to Nelnet. The main reason behind this is that back in 2018, Nelnet acquired Great Lakes. The two companies agreed to continue servicing their student loan portfolios separately, but starting last year the transfers to Nelnet kicked off and now all that’s left of Great Lakes is this page. If you want to know about the storied history of the company, you can check out this page which seems to have been created during happier times.

Complaints

The ire from customers around how this transfer has been handled is palpable. Here are a few examples:

The overriding theme is that Great Lakes seemed to know what it was doing, had the benefit of experience, and it’s been pretty difficult with Nelnet and at times has also involved the Treasury and the Education Department. I expect more of these types of issues to start popping up beginning tomorrow, unfortunately.

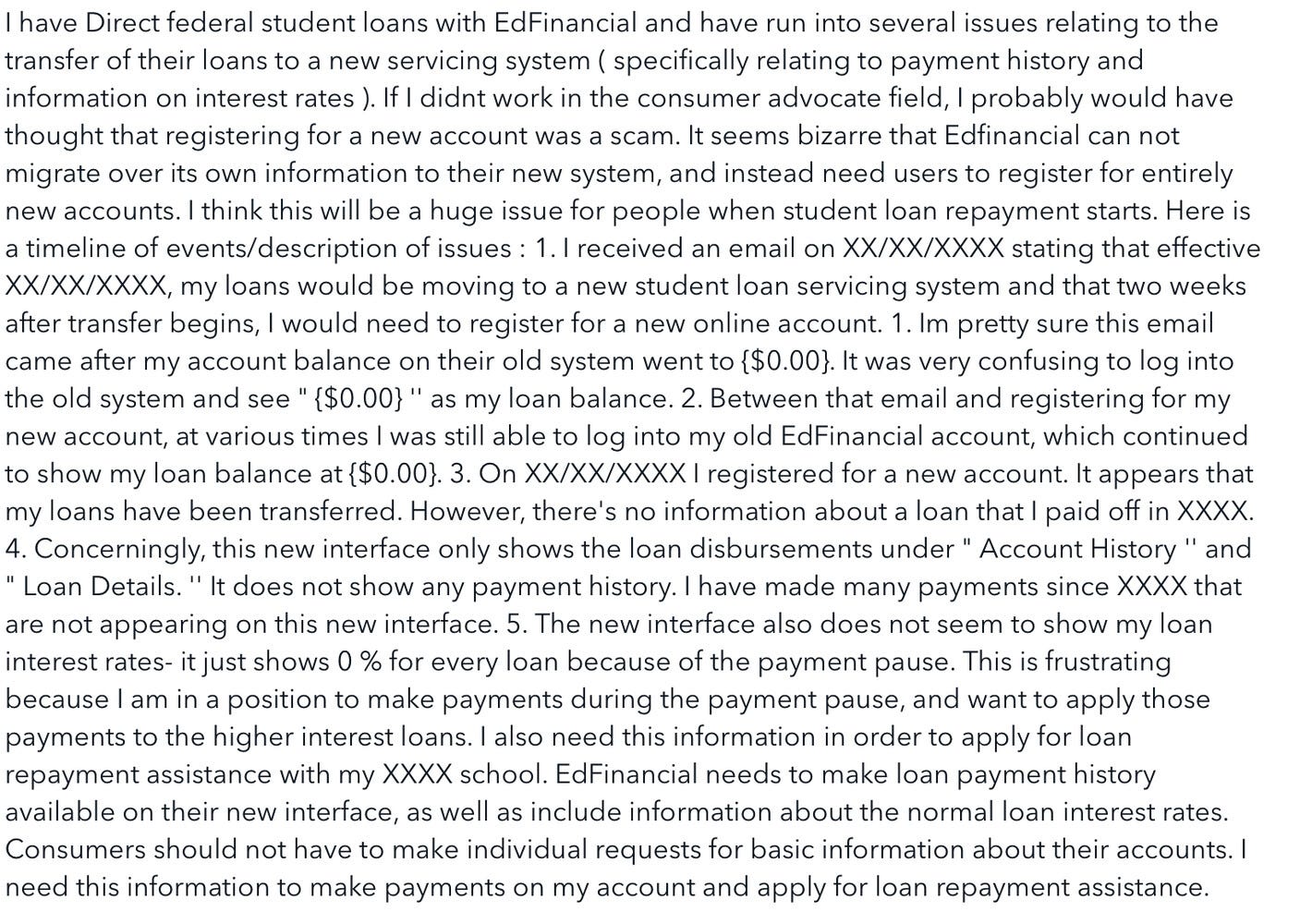

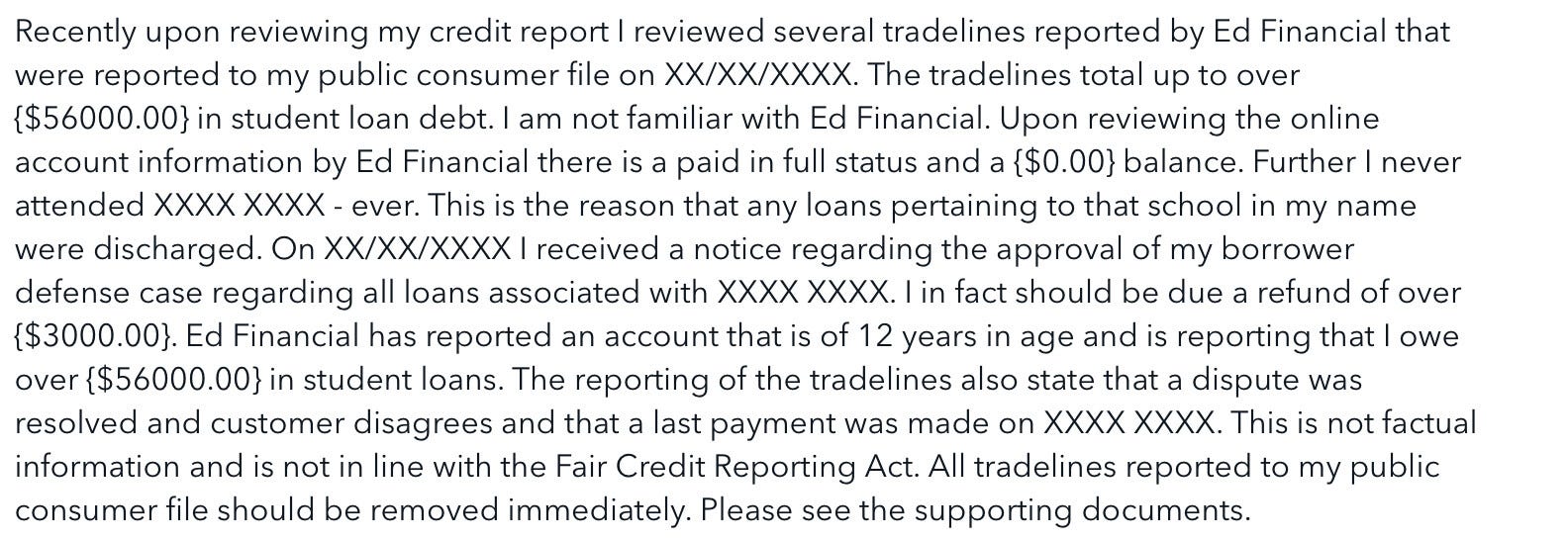

EdFinancial

The CFPB Consent Order

Despite being a servicer of federal loans, and thus clear of many of the issues that have plagued private servicers, Edfinancial couldn’t help itself and got caught with its pants down by the CFPB. Specifically, they were entrusted with handling the very delicate and very talked-about PSLF (public service loan forgiveness) program, and ended up telling a number of borrowers that they were eligible when they were, in fact not. They got a $1 million fine for their efforts coming out of a CFPB action from March of last year.

Complaints

The middle complaint is particularly noteworthy - the customer highlights an issue in their attempt to transfer to a new internal servicing system. For those who have loans with EdFinancial, pay attention to that complaint and if possible, note that you may have to do your own accounting of prior payments since it seems that for whatever reason, the transfer appears to have purged records of past payment history and has only carried forward balances outstanding.

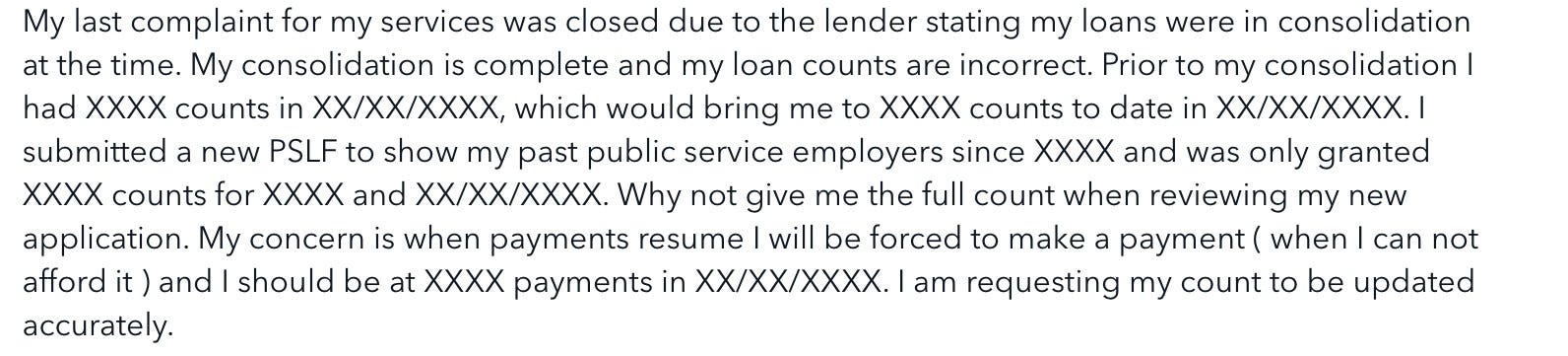

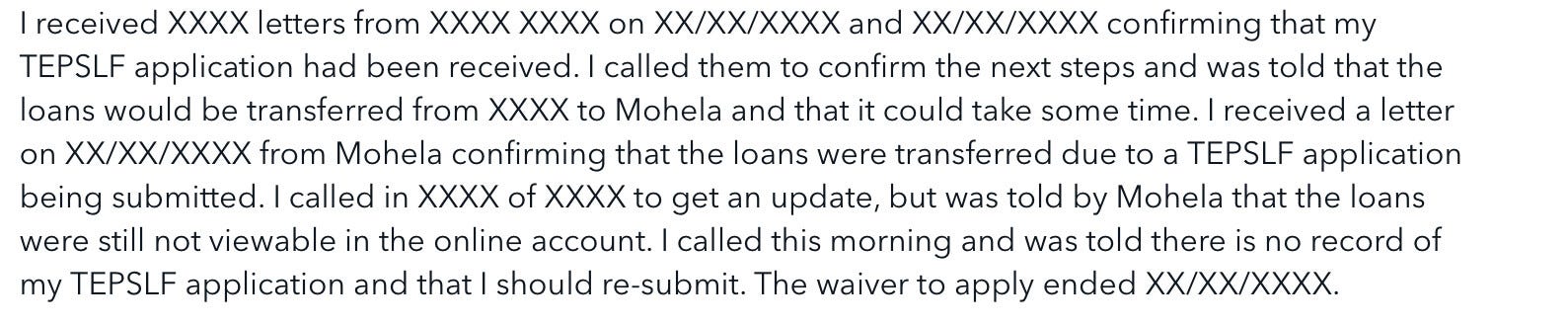

Mohela

More PSLF Drama

My personal servicer themselves! While they have been pretty good (so far) to me, they aren’t immune from horror stories either. They stand out in that they had the honor of having a US Senator (who happens to be my Senator) openly call them out for their bungling of PSLF processing. His office was deluded with complaints, which are probably on top of complaints the CFPB was getting (more on those below).

Complaints

While Senator Menendez’ complaints cited are pretty straightforward, the following are just head-scratchers:

The last complaint, it should be noted, is still in progress (being investigated by Mohela), and has been in progress for over two months now. The CFPB expects any institution that receives a complain through them to respond to the consumer within 15 calendar days.

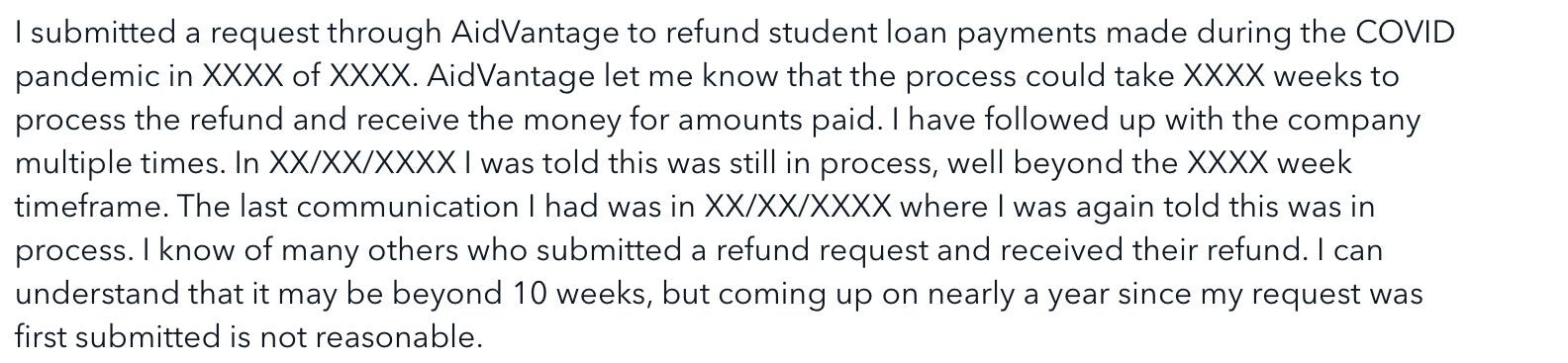

Aidvantage (aka Maximus)

Picking up where Navient left off

At the beginning of 2022, Maximus took over Navient’s portfolio of student loans (they of the $1.7 billion misleading lawsuit variety), but within three months, the backlash from borrowers was so immense in terms of the quality of servicing that the Washington Post did a piece on the saga and the issues borrowers were facing. It seems in this case, the new cop was even worse than the old cop, in some ways. This story also doesn’t end here, stay tuned for “Default Resolution Group” to see what else happened.

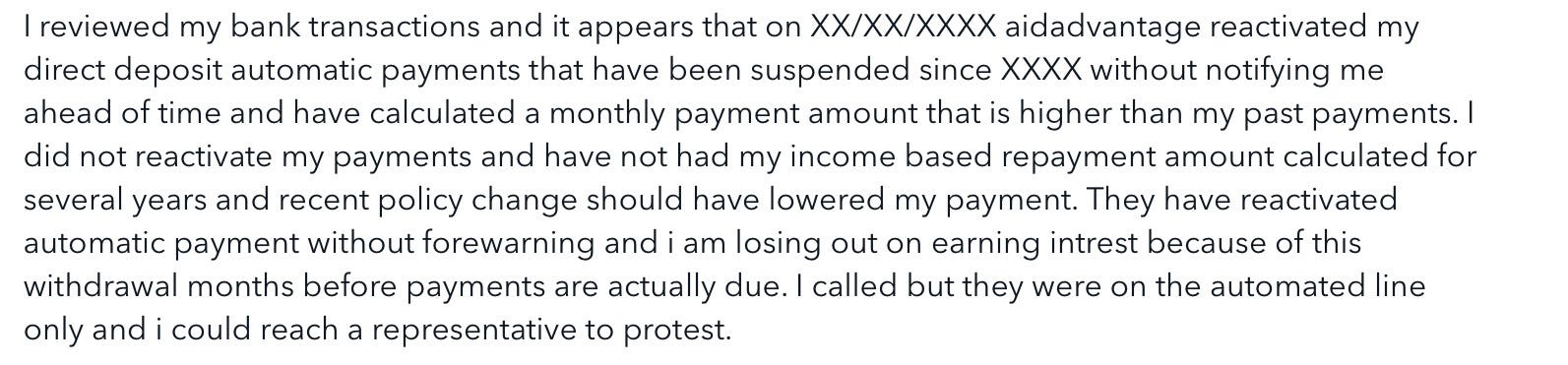

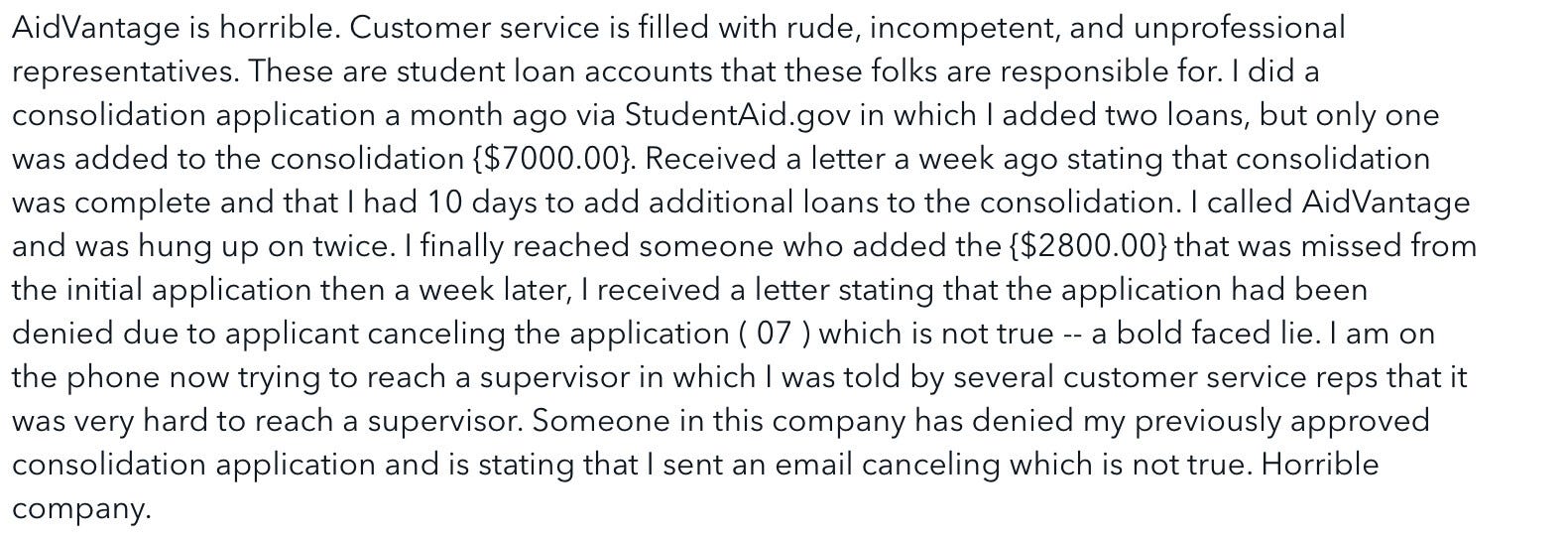

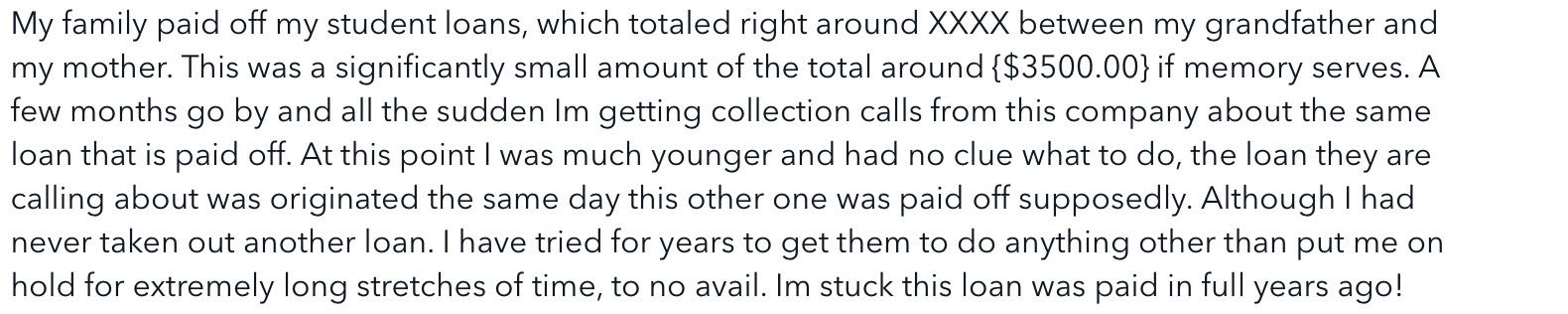

Complaints

The complaints for this company are across the spectrum, ranging from refund issues to unauthorized withdrawals to improper consolidation request handling.

OSLA Servicing

Nothing to see here?

To my shock, there’s been no major news story, no CFPB consent order, and no bungled acquisition/transfer of portfolio involving this company. OSLA stands for Oklahoma Student Loan Authority. Perhaps the locality of the coverage may be a part of why they can actually handle things somewhat competently. With that said, they too are not entirely immune to complaints.

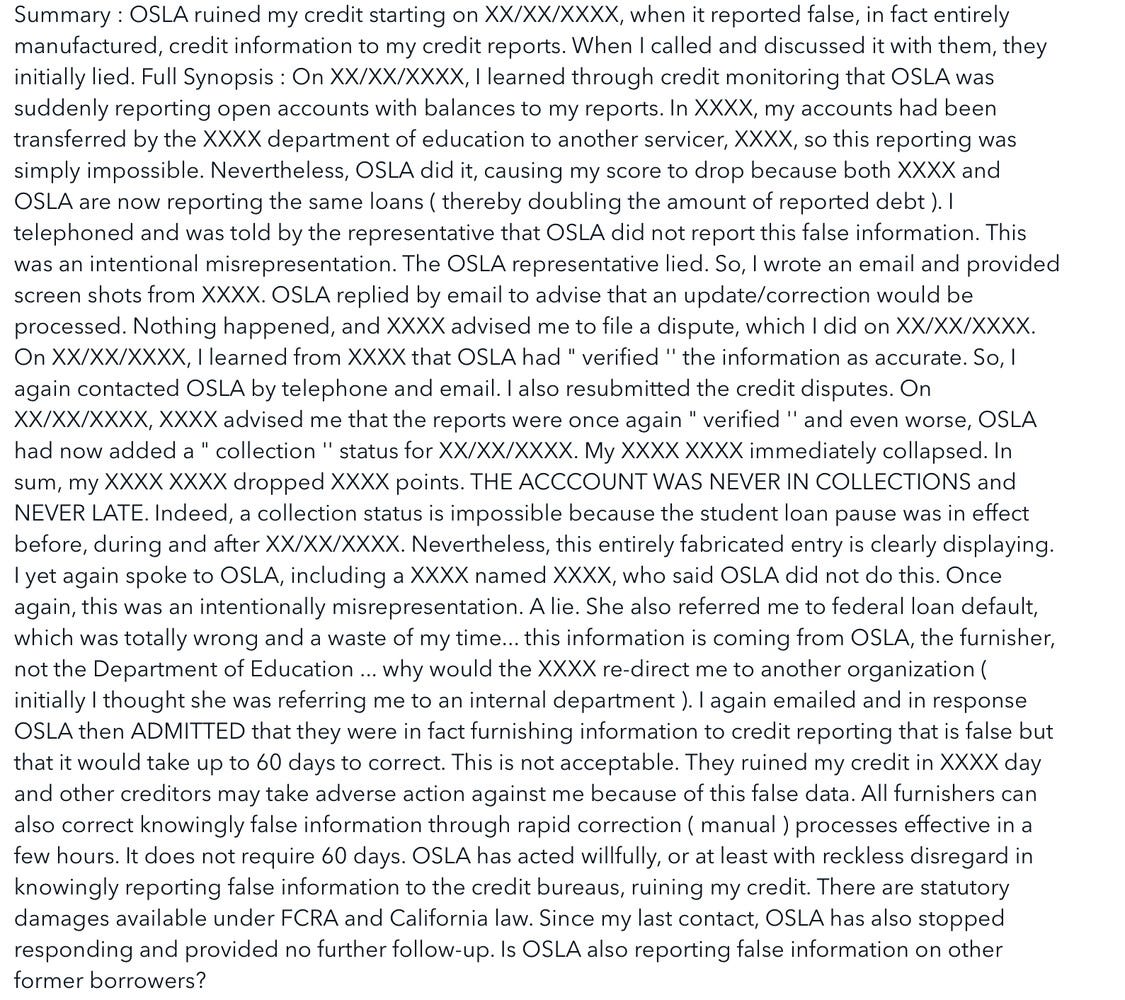

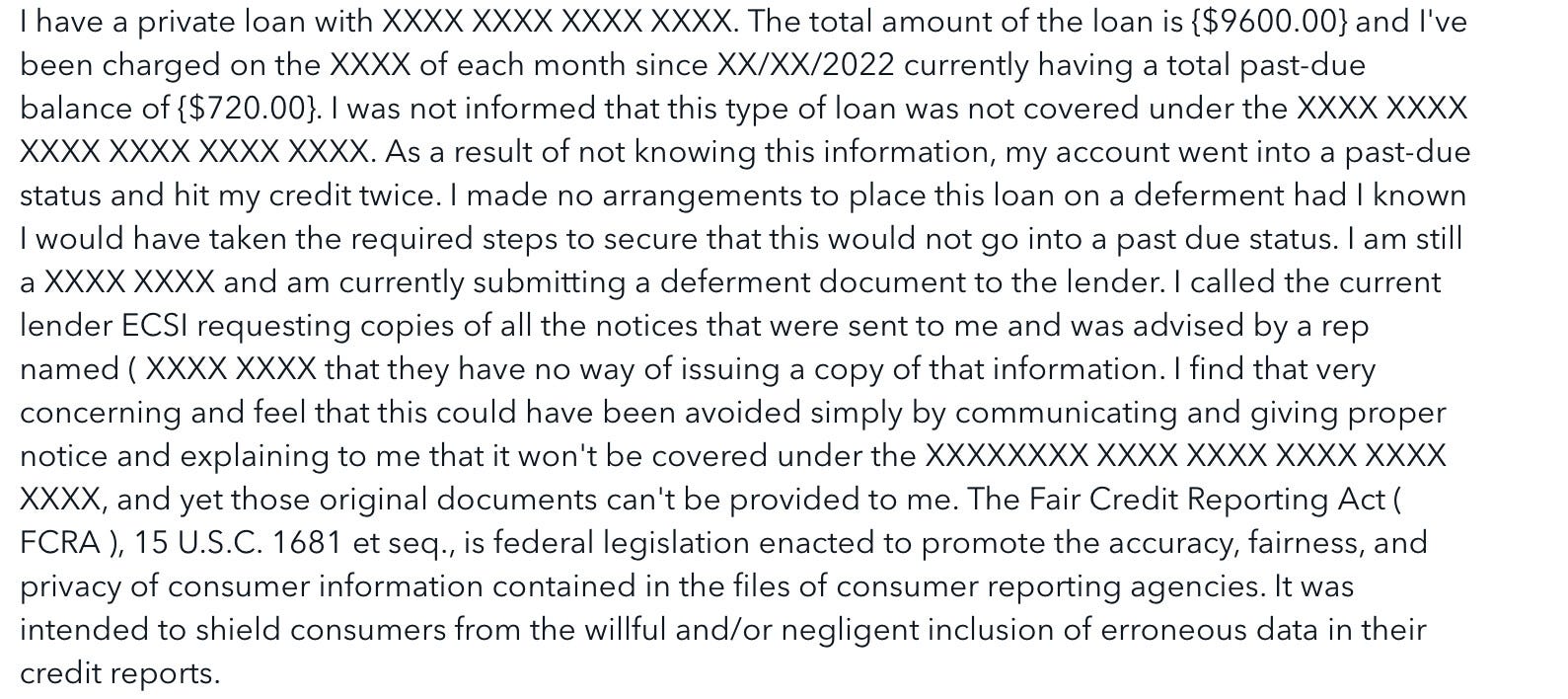

Complaints

The second one is particularly brutal. Improper credit reporting can destroy any individual’s ability to buy a home, rent, and in some cases even get a job.

ECSI

CFPB Civil Investigative Demand

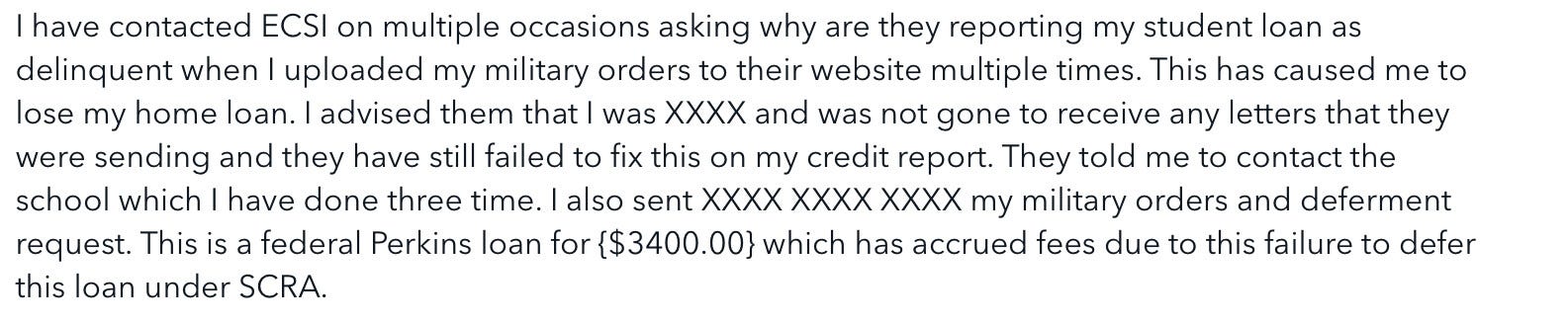

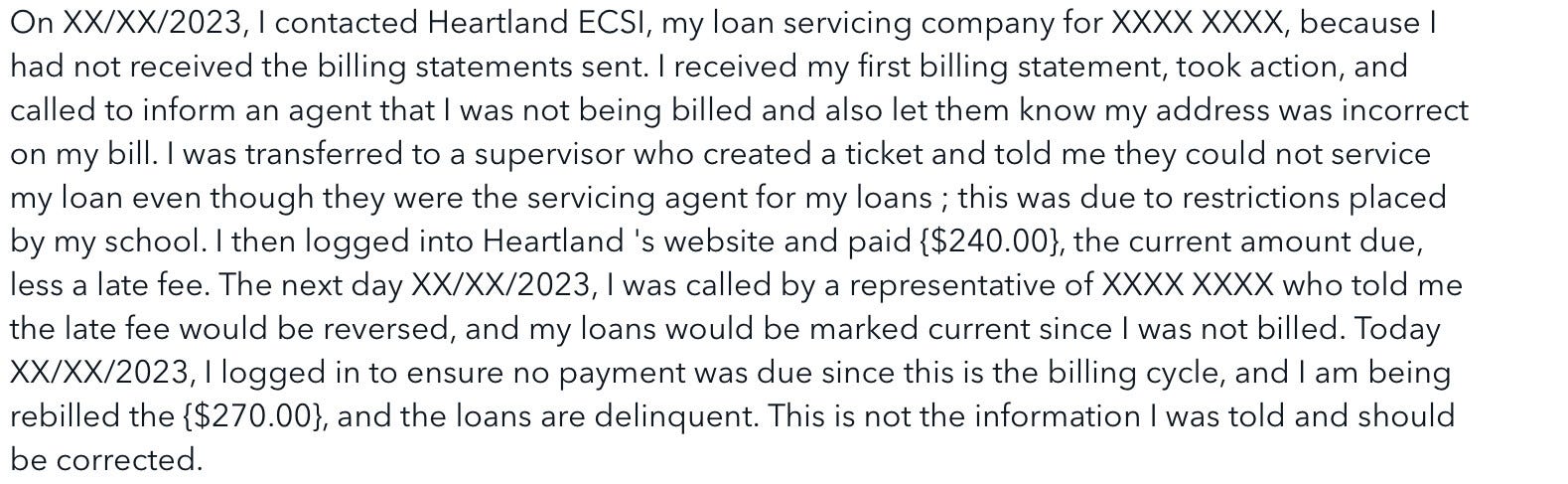

There was an interaction with this lender (ECSI, sometimes known as Heartland ECSI) and the CFPB that actually made it all the way to court. The CFPB had heard a number of complaints that compelled them to dig deeper into the practices of this company. They issued a “civil investigative demand” to be able to do so. The company responded by taking them to court, claiming the agency had no right to do so. It did not work out, as a Third Circuit judge ruled that the CFPB had the authority to enforce the demand. In the end, it all turned out to be a nothing burger as there was no enforcement action taken by the CFPB. However, this doesn’t mean that complaints aren’t en masse here either.

Complaints

The more you read these, the more you get the sense that these are not minor mistakes. Take a look at example 1 above. This person lost a home loan because of ECSI’s incompetence.

Default Resolution Group

Another Maximus Cinematic Universe Story

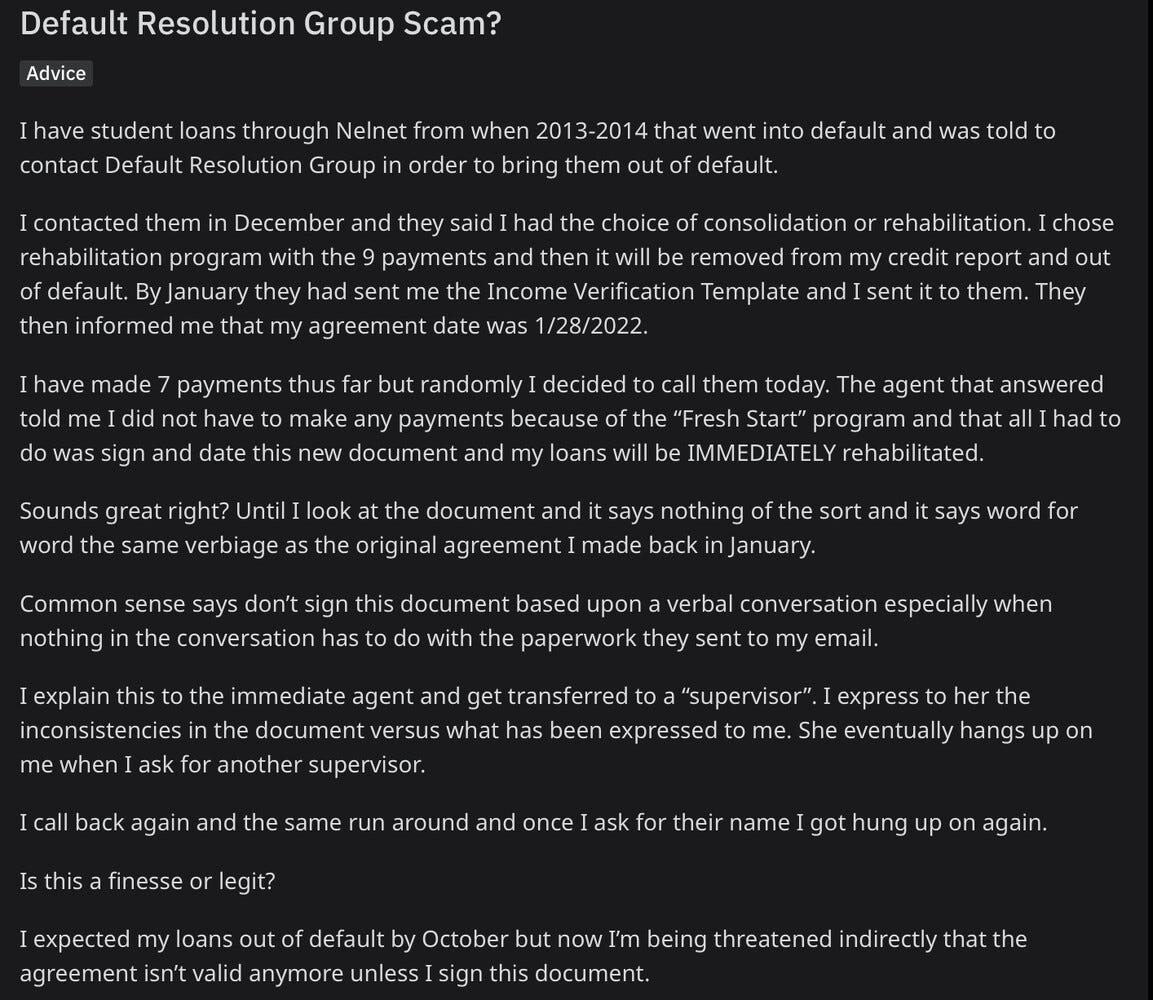

As with Aidvantage, our friend Maximus is also involved here. Forbes put out a piece that covered an investigation by several student loan consumer advocacy groups entitled “Bombshell report”. While Maximus vehemently denied the representation of the report and actually referenced the CFPB complaints, citing them as “99 out of 6 million” in a way to dismiss them, the article covered one aspect of the report that had previously gone unreported, that it is actually Maximus that is behind the call center support for this company that purports to “help student loan borrowers in default.” While it is technically managed overall by the US Department of Education, the call center servicing is all managed by Maximus. And how do they shape up?

Complaints

While I had to go to Reddit to find actual complaints about this “wing” of the Department of Education, it is interesting that the CFPB won’t accept complaints about this servicer since technically, in spite of the work they’re doing being directly supervised by the DOE, the servicing is being provided by Maximus.

The bottom line

The reason we shared this was to warn those of us who are getting ready to start paying again (if any of us stopped) to be cautious and review some of these incidents to know what you’re getting into. The media has mostly focused on the economic challenges many will have just trying to make payments, and there’s a huge debate that continues to rage about forgiveness; but what they have yet to cover is the stress and pain that terrible servicing can create which is entirely avoidable and should never be the fault of the borrower, yet here we are with all of the above and countless other examples.

Good luck to everyone out there, we’re all gonna need it.